Celebrating America’s 250th birthday, and a midyear outlook for markets.

Before we discuss the state of the markets halfway through 2026, a quick ode to America as we celebrate her 250th birthday. The “numbers guy” in me was interested in quantifying just how much America has achieved during her relatively short lifespan.

When our Founding Fathers penned The Declaration of Independence, the US population was roughly 2.5 million people (0.3% of the global population) and the size of the US economy totaled $400 million (0.7% of global GDP).

Over the ensuing 250 years, the nation has transformed itself from David into Goliath in fairly short order. Today, the US population stands at 340 million (a 136x increase from 1776) and US GDP has grown to $32 trillion (an 80,000x increase).

Along the way, the dynamism of the American economy has been the engine of global innovation, which has helped reduce poverty by 90%, improve literacy rates by 7x, increase life expectancy by 2x, and enhance the quality of life for billions of people globally (we wrote about this in more detail in 2024).

While America faces many challenges both domestically and abroad, we remain optimistic that the US remains best positioned over the long-term to create innovative and valuable products and services that will improve lives globally. As long as the US continues to embrace entrepreneurs and builders who tackle the world’s problems, those who invest in America will be rewarded.

2026 First Half Recap

As for 2026, there has been no shortage of fireworks in the markets during the first half of the year. Mr. Market was in a nervous mood in Q1, driven by a mountain of geopolitical and market related concerns. The list was long, but was headlined by the Iran conflict/Strait of Hormuz closure, concerns about AI eating software and labor, and liquidity issues in retail oriented private credit products. The S&P 500 experienced a -9% correction in March as a result.

As we wrote about in our last blog, the Q1 market sell-off coincided with an explosion in earnings growth from the AI leaders, which created an attractive entry point for investors at the end of March (faster growth at lower prices).

What ensued was the best quarter for the market since Q2 2020 (the COVID relief rally) and the 2nd best quarter since 2008. In Q2, the S&P 500 gained +15% and the tech-heavy NASDAQ rose +22%. As we wrote at the onset of the Iran conflict, savvy long-term investors should not sell stocks in the face of short-term geopolitical turmoil.

All told, the S&P 500 delivered a +10.2% return in 1H 2026 and the NASDAQ gained +13.1%. Additionally, as AI adoption accelerated this year, the number of companies benefitting from the AI supercycle expanded. In years past, the primary way for investors to benefit from AI was to invest in the Magnificent 7. This year, winners have emerged across a number of additional verticals (memory stocks, semiconductor equipment, and select pockets of energy and industrials levered to data center construction). The expanded AI opportunity set powered emerging markets (+23.8% YTD) and small caps (Russell 2000 +22.6% YTD) to new all time highs.

Over the last few weeks, the strong momentum of April and May began to fizzle out. The market hit an all time high on June 2nd and has been running in place for 5 weeks.

The question facing investors now is: was Q2 the grand finale for the AI supercycle? Or can the show go on even longer?

2026 Second Half Outlook

To answer this question, we will revisit the key points we made in our 2026 outlook. We will share what has transpired related to each of these comments, and what we expect to see for the rest of 2026.

“The clock is ticking on AI monetization… Yes, big tech companies have enough money today to fund their AI investments. But the market will only be patient for so long. If AI profits are slow to materialize while another $400bn+ of capital is invested in AI infrastructure, AI stocks could face a meaningful correction”

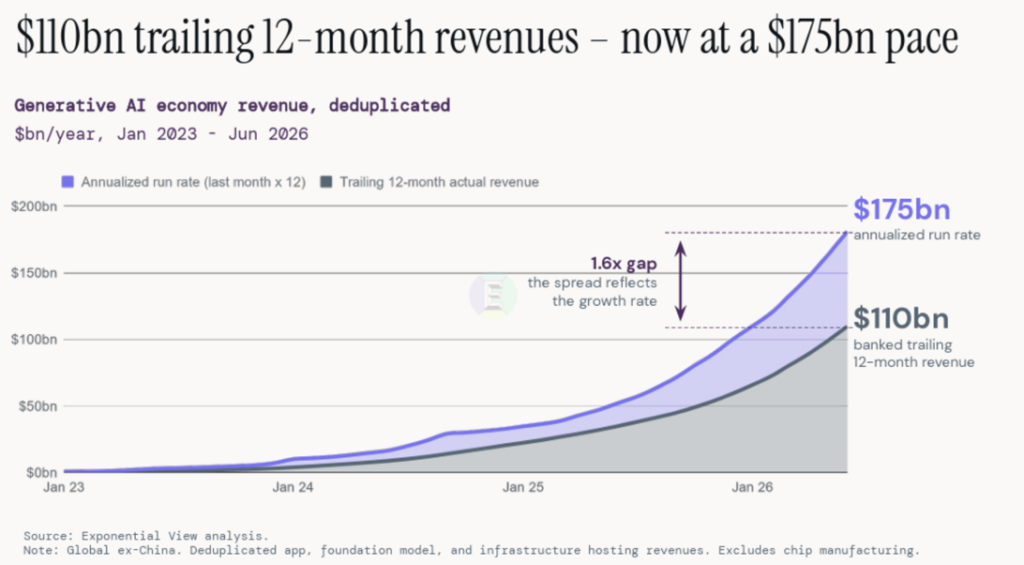

This was the biggest risk coming into 2026, and to this point it has been answered emphatically. The AI industry had a breakthrough moment for monetizing all of this AI spending. A recent analysis calculated that the AI industry is currently generating $175 billion of annualized revenue, which is more than double where we were a year ago.

This is the primary reason why the market has performed so well in 2026 despite geopolitical issues, rising inflation, and slowing economic growth.

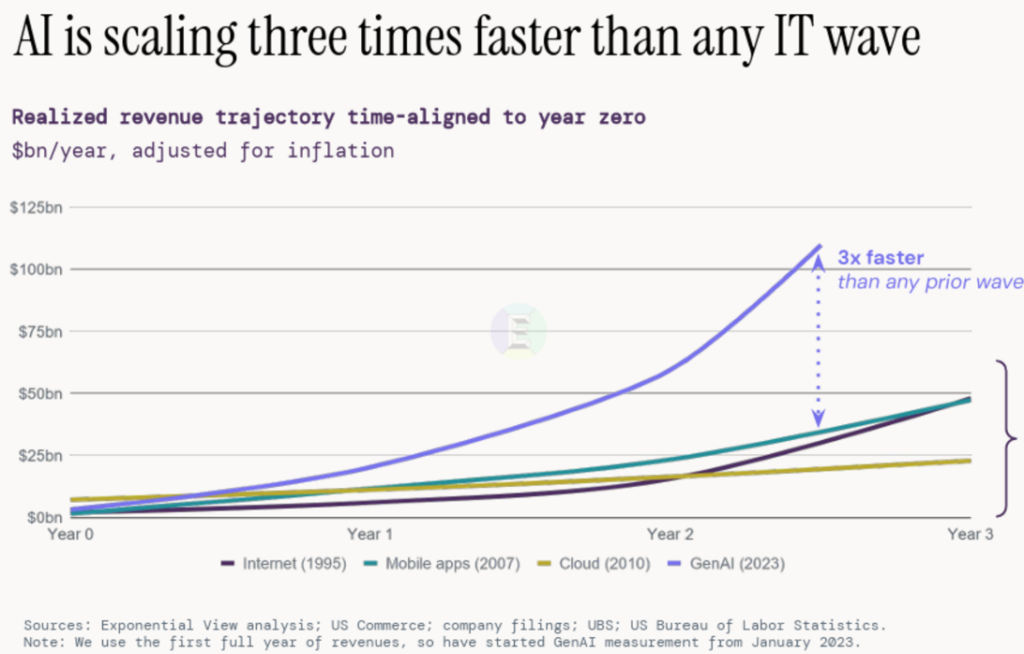

We have commented before that the speed of AI adoption has far exceeded any prior tech wave. We are now seeing that revenue generation is also happening far faster than the internet, mobile, and cloud innovation cycles. AI related revenue is 3x where these prior tech waves were at this point in their adoption cycles.

“We are bullish on AI over the long-term. AI models will continue to get better, anxiety regarding job loss will eventually subside, and AI will become a big part of everyday life, driving productivity gains globally. As such, we continue to be optimistic about venture capital and growth-oriented investments for long-term portfolios.”

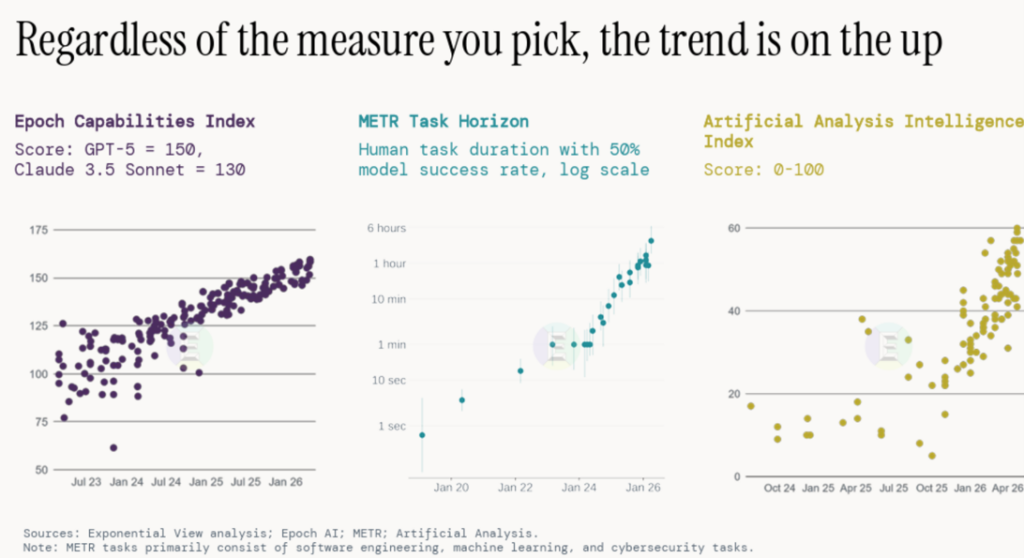

We made a few key points here. The first is that AI capabilities would continue to improve. That has certainly been the case over the last 6 months, which is why demand has grown and therefore revenue has followed.

Measured through 3 distinct metrics, AI has gotten meaningfully more effective over the last year, as shown by the dots in each analysis moving up and to the right.

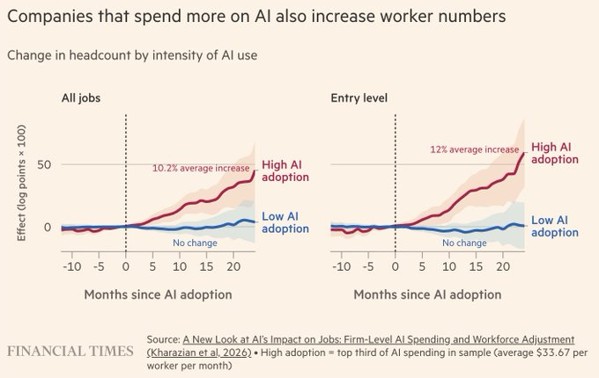

We also made a claim that anxiety regarding job loss will eventually subside. While the anxiety has not gone away (and if anything has grown), the hard data shows that companies with high AI adoption rates are actually hiring more people than companies with low AI adoption rates.

“If the economy and the stock market are reliant on AI adoption and monetization, it concerns us that sentiment surrounding AI remains so polarized. If public sentiment continues to be sour, we would expect adoption to organically slow, and a further hurdle could come from lawmakers who follow the wishes of their constituents to provide further speed bumps for the AI build-out.”

This risk has not been addressed, and unfortunately our outlook regarding AI polarization has proven to be correct. In fact, according to a recent NBC News poll, AI is less popular than many other major global figures and institutions, with a 26% approval rating.

While AI opposition has not slowed down the adoption rates by businesses, this risk has manifested itself most acutely in the pushback on data center construction. 75% of Americans oppose having data center construction near their homes. So far, 14 states have introduced moratoriums or bans on data center development.

To this point, AI opposition has not stopped the growth of the data center buildout, but it perhaps has slowed down the growth rate. Data center construction grew at a 23% year-over-year rate, which is a healthy level of growth but much lower than the last 3 years. If construction bans become more widespread, the innovation curve for AI models could slow.

“Another wildcard is IPO activity, a fairly reliable indicator of the end of bull markets. If we see a surge of IPO activity from AI leaders like OpenAI and Anthropic, that could be another warning sign that it is time to take profits.”

It is too soon to tell on this particular risk. The marquee IPO of the first half of 2026 was SpaceX, which went public at a $2 trillion+ valuation. We did not specifically call out SpaceX in our 2026 outlook, for a few reasons. While SpaceX is an AI company now, it has been around for 24 years and probably could’ve been a public company years ago. SpaceX’s core business, Starlink, is also not a direct AI play, and is profitable.

Therefore, we view SpaceX’s IPO as less relevant to this market cycle than OpenAI and Anthropic, which are consuming a significant amount of venture capital dollars and are far and away the leaders in AI market share (and spending in the AI ecosystem).

Once OpenAI and Anthropic do go public, they will need to show a path to profitability, which could lead to some rationalization of their aggressive spending plans. One can envision a scenario where spending discipline slows down the velocity of dollars through the AI ecosystem, and/or creates volatility for the broader markets once these companies are under the scrutiny of public shareholders.

OpenAI and Anthropic have both confidentially filed for their IPOs, but this does not guarantee that they will go public in 2026. We continue to have the view that once these two AI giants go public, it could be a precursor to a speedbump in the AI supercycle.

“Our base case is that the bull market remains in-tact for another year given the economic tailwinds in place currently.”

We see no reason to change our outlook at this time. The S&P 500 came into the year trading at 22x earnings. Despite being up +10% in the first half, the market is actually cheaper than it was at the start of the year (now trading at 20x earnings). Earnings growth for 2026 is now projected to be 23.3% vs. 14% at the start of the year.

Many ask if we are in an AI bubble. On a valuation basis, it is clear that we are not in a valuation bubble since the market is getting cheaper.

However, it is not out of the realm of possibility that we are in an earnings bubble. We increasingly see enterprise AI customers noting that the cost of running AI models was higher than they anticipated. Many businesses adopted the strategy of “tokenmaxxing” during the first half of the year, which means that the way to win in an AI world was to use as much AI as possible (tokens are a unit of data processed by an AI model).

This may be fine if these customers see real, tangible value from their AI spending in their business. However, AI remains a nascent technology. It is easy to envision some air pockets over the next year if some larger customers pullback or rationalize their AI spending as they learn more about the best ways to use the technology in their business.

Back to the original question – was Q2 the grand finale? While predicting what the market will do over the short-term has been a fool’s errand for Wall Street for a long time, our view (with humility) is that owning the S&P 500 at 20x earnings with 23% earnings growth is not a bad recipe for success, so our outlook is for a solid second half of 2026.

However, the risks we have noted above – societal opposition to AI, the prospect for an IPO frenzy, and the potential for AI spending moderation – remain front and center in our minds.